“Should I wait for rates to come down?”

The question has stuck with me because it wasn’t just about EMIs or affordability calculations. It was about fear. About trying to time something that no one, not economists, not central banks and not even the RBI can fully predict.

And yet, every single day, thousands of families across Mumbai’s peripheral belt are making their biggest financial decisions in the shade of that same question.

Property is never just a transaction. It is a decision made at the mid of aspiration and anxiety and right now, interest rates sit right in the middle of that intersection.

Let’s take a look at the rates

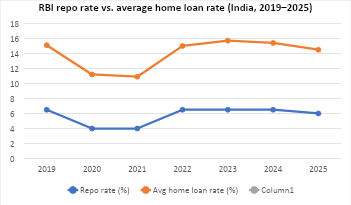

Home loan rates in India peaked around 9.5% in late 2023 after the RBI’s rate hike cycle. Since then, there have been early signals of a turn. In February 2025, the RBI cut the repo rate by 25 basis points, the first cut in nearly five years. Another followed in April.

What this means practically is that on a ₹60 lakh, 20-year loan, the difference between 9.2% and 8.5% is roughly ₹3,200 per month. That’s a child’s school fees. That’s a family grocery budget. That’s real.

The “wait and watch” trap

Here’s what I’ve seen happen again and again over six years of building in Mumbai’s extended places that buyers wait for rates to drop.

Rates drop.

Prices move up.

They end up paying more for the same flat, even on a lower EMI.

It sounds counterintuitive, but property prices and interest rates don’t always move in opposite directions especially in undersupplied micro-markets. When cheaper credit unlocks demand, inventory that was sitting quietly starts moving fast.

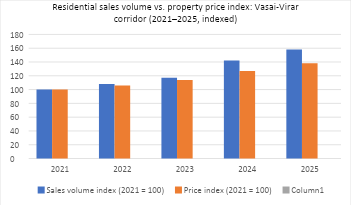

Vasai-Virar saw property prices rise approximately 38% between 2021 and 2025 during the same period when interest rates were at their highest. The demand didn’t disappear. It compressed and then released. Buyers who waited for the “perfect rate” often found the entry price had moved beyond their comfort zone.

What smart investors are doing differently

The buyers I’ve seen make genuinely good decisions aren’t the ones trying to perfect the rate cycle. They’re asking different questions and it’s not “what’s the EMI today?” but “what will this area look like in five years?”

Not “should I wait for 7.5%?” but “am I buying in a place where infrastructure is arriving?”

Along the Mumbai-Ahmedabad highway corridor, you have a confluence of factors that are rate-agnostic: the Virar-Alibaug multimodal corridor, the MTHL ripple effect, improved rail connectivity these are structural demand drivers that compound regardless of where the repo rate sits.

Just remember,

“The best time to buy was always a year ago. The second best time is when you’re ready and not when the rate is perfect.”

If you’re buying a home to live in then the interest rate conversation matters far less than you think because you’re buying stability, you’re buying the feeling of not renewing a rental agreement every eleven months instead you’re buying the right to paint your walls whatever colour you want.

A 50-basis-point rate movement matters. But so does living in a neighbourhood with a school your kids can walk to, a station 10 minutes away, and a building that actually gets delivered on time.

At Techton Lifespaces, we’ve always believed the best investment is a well-located, well-built home bought when you’re genuinely ready. Rates are a tailwind or a headwind, never the destination. If you’re evaluating a decision right now, we’d love to help you think it through not just sell you a flat. That’s a promise we’ve held since 2019, and it remains unchanged.